Trade

Basic

Futures

Futures

Hundreds of contracts settled in USDT or BTC

TradFi

Gold

Trade global traditional assets with USDT in one place

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Participate in events to win generous rewards

Demo Trading

Use virtual funds to experience risk-free trading

Earn

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and enjoy airdrop rewards!

Futures Points

Earn futures points and claim airdrop rewards

Investment

Simple Earn

Earn interests with idle tokens

Auto-Invest

Auto-invest on a regular basis

Dual Investment

Buy low and sell high to take profits from price fluctuations

Soft Staking

Earn rewards with flexible staking

Crypto Loan

0 Fees

Pledge one crypto to borrow another

Lending Center

One-stop lending hub

VIP Wealth Hub

Customized wealth management empowers your assets growth

Private Wealth Management

Customized asset management to grow your digital assets

Quant Fund

Top asset management team helps you profit without hassle

Staking

Stake cryptos to earn in PoS products

Smart Leverage

New

No forced liquidation before maturity, worry-free leveraged gains

GUSD Minting

Use USDT/USDC to mint GUSD for treasury-level yields

More

How will the stock and bond balance shift after the holiday?

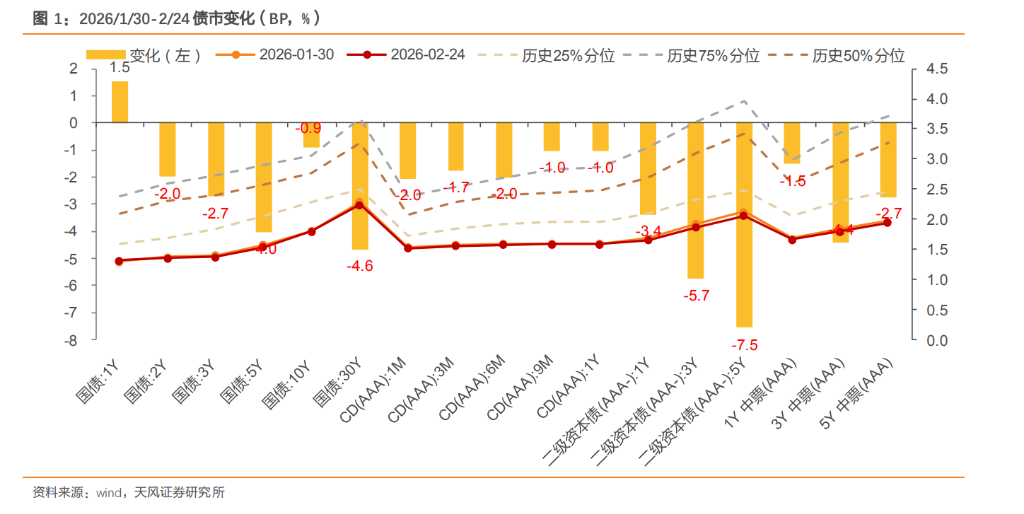

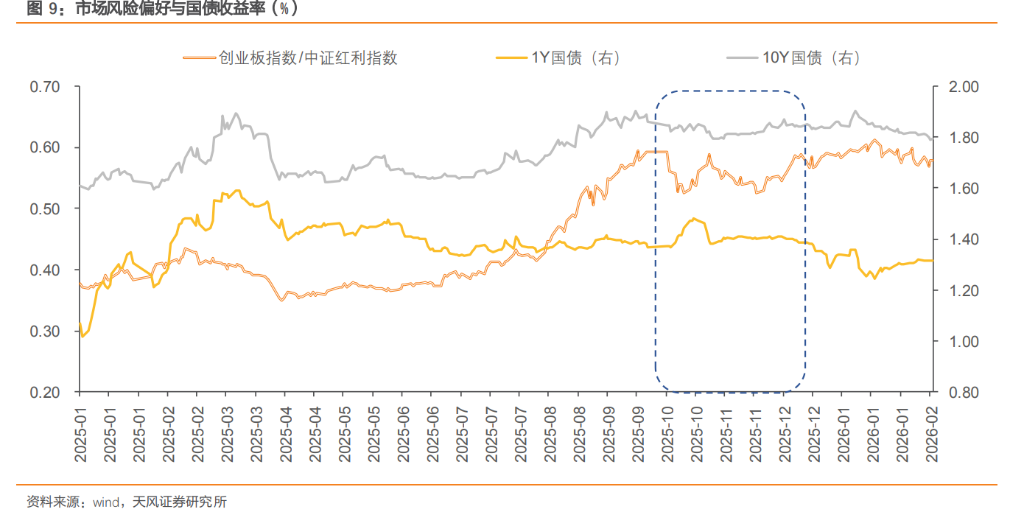

Since the beginning of the year, the relationship between stocks and bonds has experienced a progression of “strengthening tug-of-war → divergence and convergence → rebalancing”: At the start of the market, A-shares posted a “good start,” with the technology growth sector leading; bond markets declined consecutively, highlighting the “tug-of-war” effect between stocks and bonds. In mid to late January, stock gains slowed, bond markets oscillated and recovered, and the divergence and convergence continued. Since February, bonds have performed relatively strongly, while stocks are not weak; bond pricing shows significant driven features from allocation, and supported by dividend sectors, the overall stock market remains resilient. After the Spring Festival, how will the balance between stocks and bonds shift? This article focuses on that.

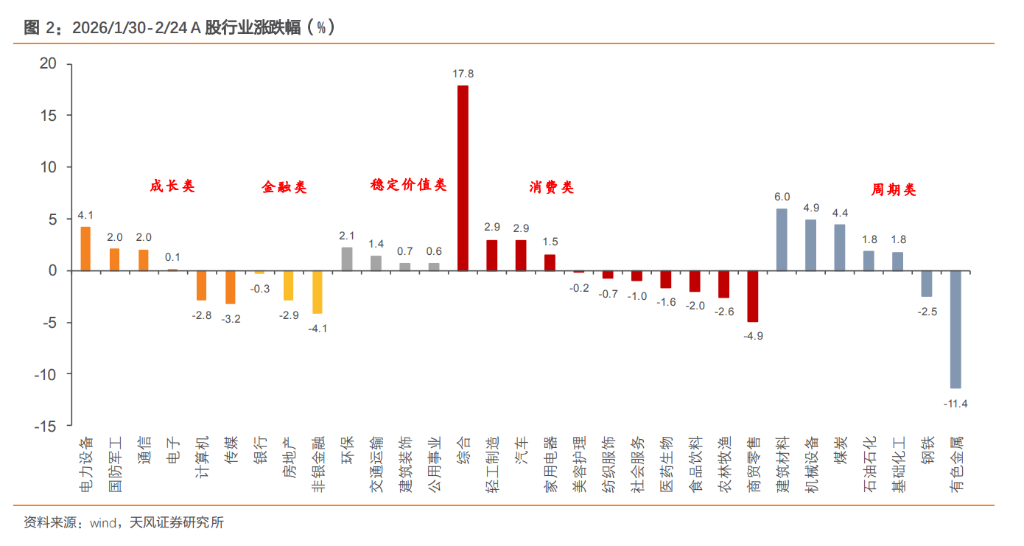

Since February, the stock and bond markets have exhibited characteristics of “bonds strong, stocks not weak.” Traditionally, before the holiday, due to ample liquidity and risk aversion, a “bond strong, stock weak” pattern appears. However, this year, expectations of a “spring rally” in stocks have increased and arrived earlier than usual. Meanwhile, the central bank maintains balanced and stable liquidity conditions. Under style switching, broad-based indices still maintain gains. Therefore, recent markets are not following a single risk-avoidance pattern but have formed a situation where both stocks and bonds are supported, with intensified competition, leading to a divergence in narratives and a weakened “tug-of-war” effect.

In bonds, January PMI data fell unexpectedly, liquidity remains balanced and loose, and the market favors dividends and defensive sectors, reflecting risk-averse sentiment that has somewhat eased pressure on bonds. Coupled with ample funds in banks, insurance, and other allocation sectors, long-duration rate bonds receive some support, leading to oscillations and warming in bond markets.

In stocks, although equity funds rotate among different styles and sectors, broad indices still trend upward. Recently, market risk appetite has marginally declined, with a shift toward dividend styles. Funds tend to flow into high-dividend, consumer, and defensive sectors, while growth sectors have experienced some pullback.

Additionally, the style shift in stocks is driven by factors such as the cash flow revaluation from year-end dividend payouts. From December 1, 2025, to February 13, 2026, a total of 294 companies in the A-share market paid dividends, totaling approximately 389.82 billion yuan, with banks remaining the main recipients. This dividend feedback provides a certain cash flow value in volatile markets, increasing the attractiveness of high-dividend sectors.

Combining style shifts with institutional behavior and changes on the liability side: recently, stocks are gradually shifting from growth to dividend styles, indicating that the market may be more cautious about economic growth and policy expectations, often accompanied by a decline in risk appetite, prompting funds to seek “fixed income-like” assets.

(1) Banks: focus on the “tug-of-war” between credit and bonds

Currently, dividend style dominates, resonating with banks’ asset-liability conditions. In January, bill rates remained low, credit issuance was insufficient, and combined with the “opening red” of deposits, bank liabilities are ample, increasing bond allocations.

(2) Insurance: focus on OCI accounts and dividend substitution

In the early stage of dividend style (market risk aversion), insurance funds may increase both stocks and bonds, with no obvious drain on bonds. If dividend style intensifies, it could trigger a migration of insurance funds from bonds to stocks.

(3) Wealth management: relatively neutral impact on bonds

Wealth management funds connect household risk preferences with capital markets. Due to small fluctuations and high dividends in dividend styles, they are suitable as a “safety cushion” for equity participation. Wealth management subsidiaries may increase yields through public funds, private placements, or directly via dividend ETFs, aiming to boost returns while controlling drawdowns. The main allocation remains in bonds; equity participation in dividend styles does not directly withdraw bond funds but may expand overall wealth management scale due to performance growth, indirectly supporting bond stability.

2.1. Growth style dominance, clear “tug-of-war” with stocks and bonds

During periods when growth style prevails, it is usually accompanied by strong industry cycle expectations, policy support, or technological breakthroughs, which systematically boost risk appetite. Funds tend to flow from safe assets like bonds and dividend stocks to high-risk, high-elasticity assets. Institutional behavior shows that "fixed income + " products and hybrid funds tend to reduce bond holdings and increase stock positions, to some extent bearish for bonds. If inflation expectations rise, investors demand higher term premiums to compensate for risks, potentially widening term spreads.

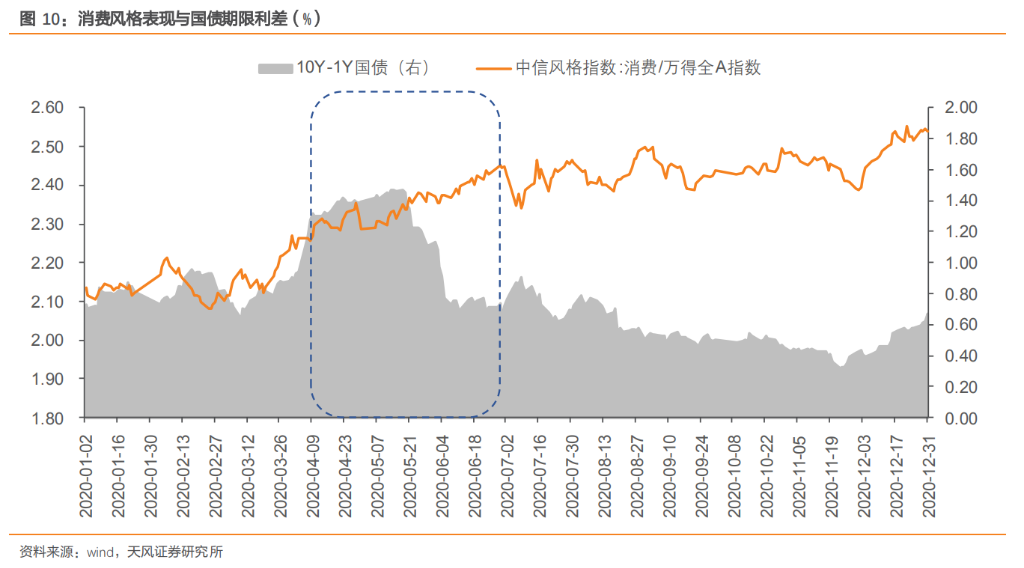

2.2. Dividend style dominance, risk aversion increases

In periods favoring dividends, economic endogenous momentum recovers slowly, macro policies remain steady, and risk appetite declines. Funds shift from high-risk, high-elasticity growth sectors to more stable “fixed income-like” assets, such as bond funds, money market funds, and wealth management products, creating incremental bond demand and often leading to bond market strength.

2.3. Consumption style dominance, neutral to slightly bearish on bonds

When consumption style dominates, economic growth expectations remain stable, supported by policies promoting consumption and easing monetary policy. Market risk appetite gradually rises, profitability and prosperity of consumption sectors improve, and some risk-averse funds move from bonds to stable, high-dividend consumer stocks, exerting some pressure on bonds.

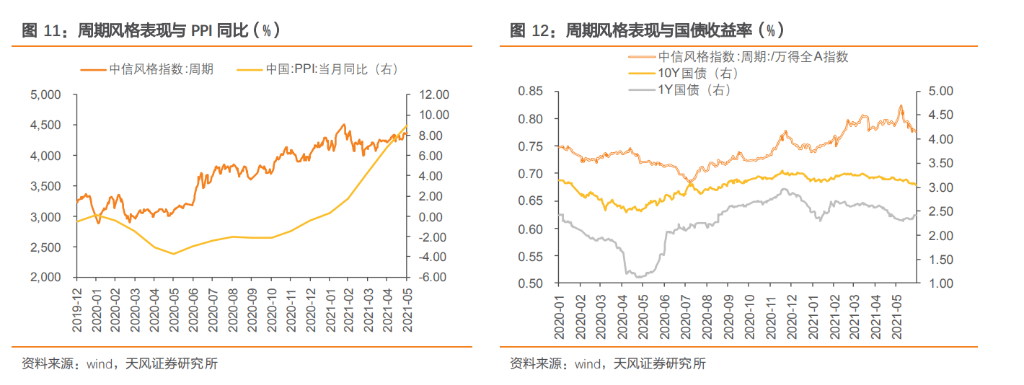

2.4. Cyclical style dominance, inflation pushes long-term interest rates higher

In periods dominated by cyclical styles, economic fundamentals improve, often with inventory cycles, rebound in fixed asset investment, and rising industrial prices. Expectations of economic recovery and corporate earnings boost risk appetite, driving funds from bonds to cyclical equities. The rise in inflation expectations, marked by PPI increases, pushes up the long-term interest rate center, leading to a general rise in rates and potential policy easing cooling, which may pressure long and ultra-long rates, requiring caution in long-duration bond holdings.

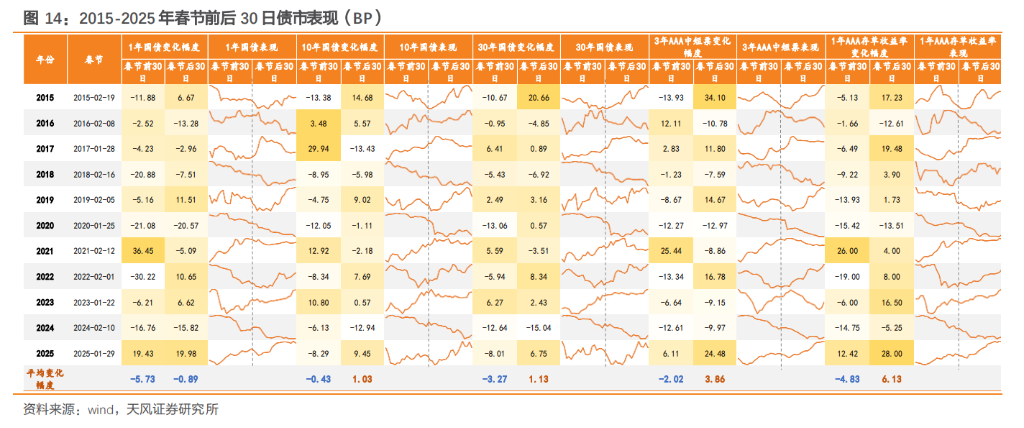

In early February, we reviewed the seasonal pattern of the stock-bond relationship in “Before the holiday, bonds stable; after, stocks warm?” (2026.2.3). Based on actual performance before the 2026 Spring Festival, the market trend remains consistent with previous observations.

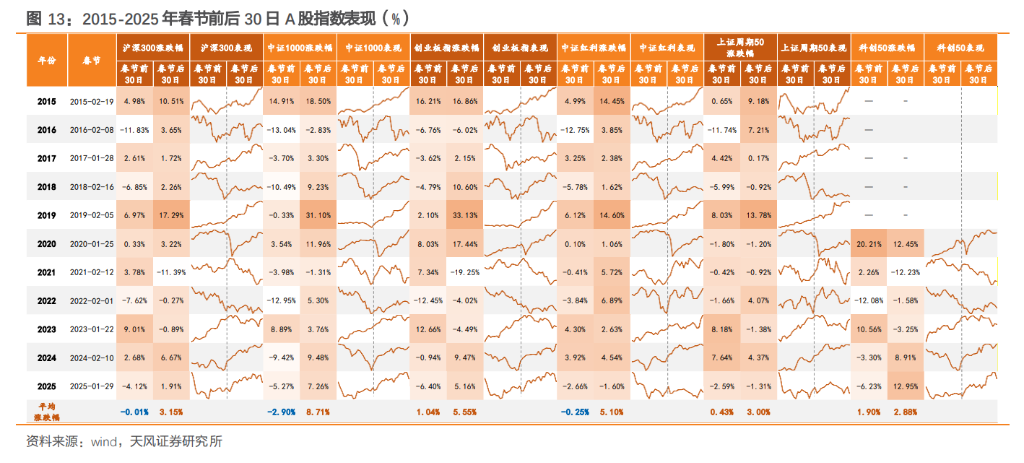

Looking at historical patterns from 2015-2025, the Spring Festival is a key style dividing line: in the 30 days before the festival, stock movements tend to be volatile, with a defensive bias, favoring dividend styles. Defensive sectors like banks, food and beverages, building materials, and petrochemicals perform well. During this period, bonds usually perform better, with yields declining, supported by central bank open market operations maintaining liquidity and financial institutions’ strong bond demand at the start of the year.

In the 30 days after the Spring Festival (2015-2025), the probability and average gains of the stock market increase. Liquidity improves, funds flow back, risk appetite rises, and policy expectations for the “Two Sessions” may heat up. The style switch in this period occurs in about 81.82% of years, with increased market activity, higher success rates for small-cap and growth styles, and sector rotations from defensive to offensive.

Post-festival, bond markets show divergence, with some risk of correction. As economic activity normalizes and key meetings approach, market debates over recovery strength and policy direction intensify, leading to increased volatility and rate adjustments, with rates tending to rise rather than fall.

Regarding the style shifts and stock-bond relationships after this year’s Spring Festival, we consider different scenarios:

(1) Scenario 1: Dividend continuation, growth weak rebound, weakened “tug-of-war”

If post-festival data shows weak consumption and real estate recovery below expectations, risk appetite remains low. Long-term funds like insurance and social security, driven by “asset scarcity” and rigid liability costs, continue favoring high-dividend sectors (utilities, banks, transportation). Growth sectors, having peaked early in spring 2026, show only weak rebounds after initial declines, lacking earnings support, with limited profit effects. Bonds, under weak economic recovery and a preference for dividends, see reduced absorption of bond yields, with limited upside in long-term yields and potential oscillation around key levels, focusing on coupon strategies and spread compression opportunities.

(2) Scenario 2: Active growth sectors, strengthened “tug-of-war”

If the Two Sessions signal strong policy support and economic data in January-February show a “good start,” liquidity remains ample, risk appetite genuinely rises, and technology growth sectors (AI, semiconductors) and cyclical sectors (resources) rebound. Dividend sectors may underperform or even decline in absolute terms, with funds shifting from defensive to high-elasticity growth stocks. Bonds may face risks: rising risk appetite could lead to bond sell-offs, especially if pre-holiday coupon demand turns into profit-taking after the festival, prompting rebalancing. Additionally, continued “money moving” from deposits to non-bank savings, funds flowing out of fixed income products, could reduce bond supply and increase volatility, with long bonds under pressure and short bonds remaining stable amid liquidity easing. Leverage strategies may be advantageous, but attention to structural opportunities is necessary.

(3) Scenario 3: Cyclical return, inflation expectations push long-term rates higher

If early 2026 data exceeds expectations, with PPI turning positive and core CPI rising above 1%, signaling a trend of price improvement, and policy signals are positive, some cyclical sectors (metals, chemicals, petrochemicals) may lead gains. The core market concern shifts from “growth expectations” to “inflation expectations,” with supply constraints and moderate demand recovery. Key price indices like GDP deflator and PPI will attract attention, and rising inflation expectations will push up long-term rates, possibly leading to a pause or reversal in monetary easing, requiring caution in long-duration bond holdings.

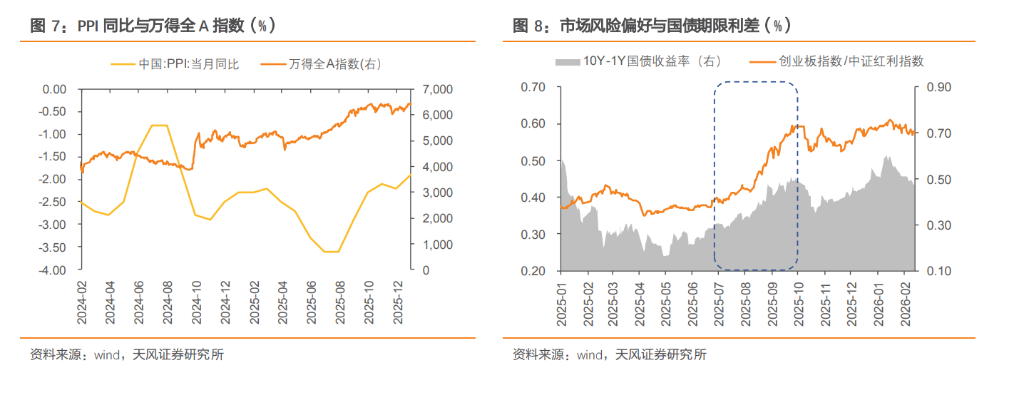

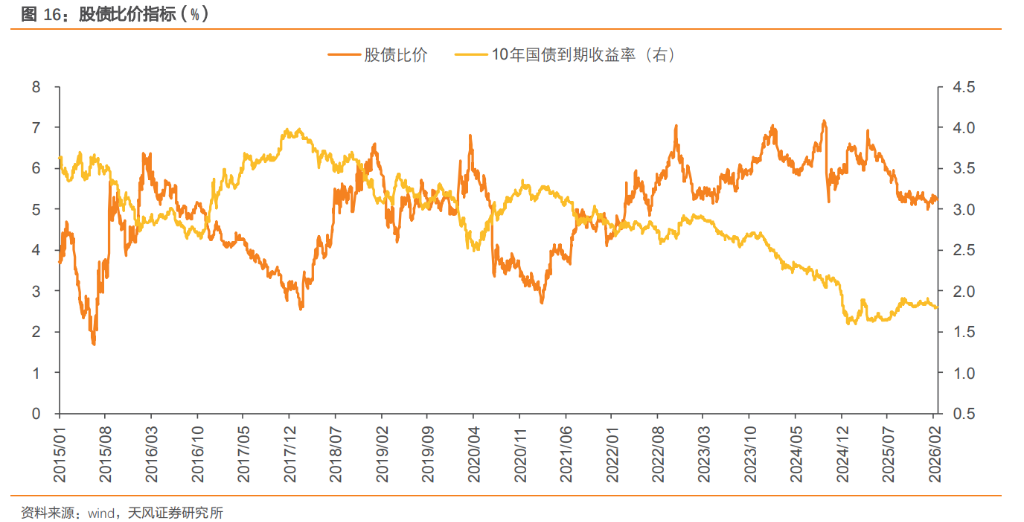

Overall, these style shift scenarios need to be confirmed gradually through high-frequency indicators. From the perspective of asset pricing, the stock-bond spread directly reflects the relative valuation and allocation efficiency between the two, serving as an important window into market balance. During dividend dominance, spreads tend to stabilize or narrow slightly without a clear trend; during growth dominance, risk appetite rises, and spreads usually trend narrower. As of 2026/2/24, the PE of the CSI 300 index reached 14.2x, at a relatively high percentile historically, indicating overall high valuation.

Further, considering the stock-bond yield ratio, bond yields are at historic lows, with the 10-year government bond yield around 1.80%, keeping the stock-bond risk-return ratio within a reasonable range, roughly at the 53.5th percentile over the past decade. Notably, although the spread indicator has recovered from undervaluation to a neutral, reasonable level, the relative attractiveness of stocks versus bonds may still exist. Future focus should be on economic data, policy signals from the Two Sessions, risk appetite, and micro capital flows to adjust style switching timing and flexibly manage stock and bond exposures.

Source: Tianfeng Securities

Risk Warning and Disclaimer

Market risks are inherent; investments should be cautious. This article does not constitute personal investment advice and does not consider individual user’s specific investment goals, financial situation, or needs. Users should consider whether any opinions, views, or conclusions herein are suitable for their circumstances. Investment is at their own risk.